Explore the ever-evolving Australian Property Market, where resilience and challenge intersect. From shifting interest rates to surging rental demands, discover the nuances shaping the nation’s real estate landscape in 2024.

The Reserve Bank of Australia (RBA) has maintained the cash rate at 4.35 percent at there meeting on Tuesday, 7th May 2024, even though there has been a slight increase in inflation according to the consumer price index (CPI) figures for the March quarter.

It comes as no surprise to many economists that the RBA chose to keep the rate unchanged, as they have been anticipating such decisions throughout the year.

“RBA is going to sit and wait and see what unravels,” says Domain chief of research and economics Dr Nicola Powell.

“I would be very surprised if we see a rate hike from the RBA [this year],” she says. “If inflation remains sticky for longer, that’s probably when they’re more likely to make a rate hike.”

Source: Domain

Table of Contents

Key takeaways

- Higher interest rates may cool property buying but price growth continues, led by Perth.

- Tight vacancy rates and limited new construction are pushing rental prices upwards, particularly in student areas.

- Stage 3 tax cuts may influence investment decisions for low and middle-income earners.

In the March 2024 quarter, the quarterly Consumer Price Index (CPI), which serves as an indicator of inflation, increased by 1 percent, surpassing the previous quarter’s 0.6 percent. Despite this rise, annual inflation dropped to 3.6 percent, still exceeding the Reserve Bank of Australia’s (RBA) target range of 2-3 percent but significantly lower than the peak observed in December 2022.

According to Michelle Marquardt, the head of prices statistics at the Australian Bureau of Statistics (ABS), “While prices continued to rise for most goods and services, annual CPI inflation was down from 4.1 per cent last quarter and has fallen from the peak of 7.8 per cent in December 2022,”

Though Inflation continues to be high while showing signs of easing, these high interest rates are set to establish a more sustainable balance as inflation still weighs on the overall cost of living.

“The central (RBA) forecasts, based on the assumption that the cash rate follows market expectations, are for inflation to return to the target range of 2–3 per cent in the second half of 2025, and to the midpoint in 2026.” – According to a Statement by the Reserve Bank Board.

Consequently, the continued high-interest rates will likely place certain barriers to large property purchases by limiting buyers borrowing capacity.

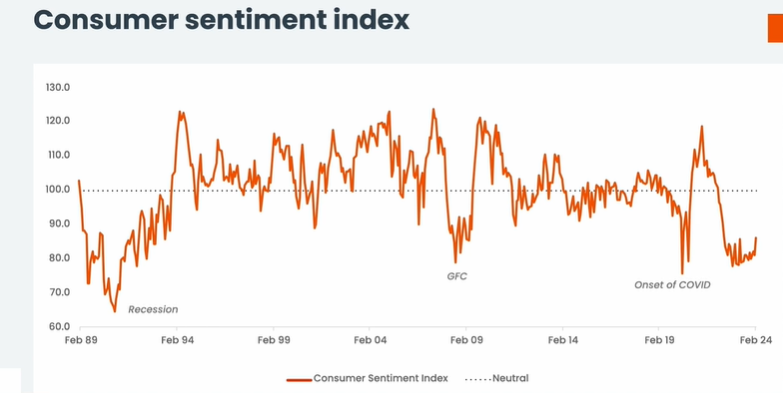

Supporting this outlook, a National Australia Bank (NAB) report analysing CoreLogic data reveals a lower-than-average Consumer Sentiment Index. This indicates that there is a persistence in spending. The higher the consumer sentiment index, the more confident investors are to make decisions on large financial commitments.

Image source: CoreLogic

Notably, The Australian Bureau of Statistics (ABS) projects the cash rate to remain unchanged until at least November 2024. This is due to slower inflation compared to other countries and Australia’s strong job market. Narrow yield differentials between saving and investing may further incentivize saving over property investment until interest rates stabilise.

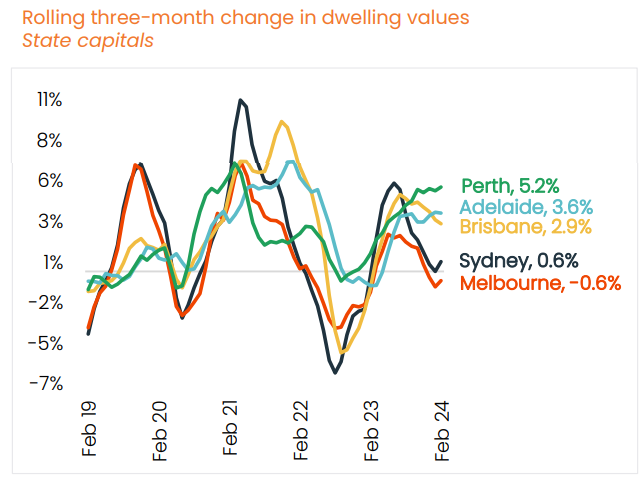

Property Asking Prices and Values

Asking prices, a real-time indicator of market sentiment, show continued growth across most Australian capital cities despite economic uncertainty. By tracking property market trends in asking prices, we can predict where actual property prices might be headed. If sellers are confident, they may set higher asking prices, anticipating strong demand. Despite the uncertainty in macroeconomic activities, property asking prices continue to increase in all sectors of Australia.

Perth leads the growth rate at 5.2%, while Sydney and Melbourne are experiencing a plateau. This resilience can be attributed to the ongoing supply-demand imbalance and anticipated rise in net overseas migration.

Source: Corelogic

Housing values in Australia continue to show resilience against high interest rates and high costs of living. This strength can likely be attributed to two key factors: a persistent imbalance between housing supply and demand, and an anticipated increase in net overseas migration to Australia.

Houses are selling faster than apartments, with minimal discounting and shorter days on the market.

Persistent Rental Market Challenges

Australia faces tight vacancy rates, further squeezing rental supply and pushing rental yields upwards. This trend is likely to worsen due to strong migration rates.

This trend is likely to intensify due to strong migration, particularly in inner-city areas popular with international students. These areas have been significantly impacted by population growth.

However, some stability is expected in rental income for areas near universities in cities like Sydney and Melbourne. The sustained demand from this demographic should provide some buffer.

Source: Corelogic

While the Australian government’s recent initiative to limit international student visas aims to alleviate these pressures, its impact is likely to be moderate in the short term. Limited new construction entering the market in the medium term further strengthens the upward trend in rental values.

Domains Chief of Research & Economic Dr Nichola Powell adds that growing rent prices will continue to be “a thorn in the side of the CPI”.

“Rent is the largest single component that goes into inflation, and we’ve seen extraordinary rates of rental growth,” she says.

The Domain Rent Report indicates a quarterly increase of 5 percent and an annual increase of 10.5 percent in capital rents.

According to the March CPI quarterly report from the ABS, rents were identified as one of the primary drivers of the inflationary uptick.

Limited new construction being approved

New home approvals dipped 1% in March, according to the Australia Bureau of Statistics data released on Monday. The report showed 12,850 dwellings receiving the green light for construction.

March’s dwelling approvals data falls significantly short of the annual target of 240,000 needed to achieve the federal government’s ambitious goal of building 1.2 million well-located homes by June 2029.

Stage 3 Tax Cuts

The new stage 3 tax cuts initiative has been proposed to decrease the tax rate for Australians earning between $18,201-$45,000. This will help ease the cost of living pressure for low-income earners by increasing their purchasing power, especially on rents and mortgages as this is a large monthly consumption sector.

In addition, the new tax cut proposal will add another tax bracket, meaning that Australians who earn between $135,001-$190,000 will now need to pay a 35% tax rate compared to just 30% before. Individuals in this tax bracket are likely to have an increased demand to purchase investment property to cut down on their taxes. Earners in the $190,000+ bracket would still retain a high demand for investment property as their tax rate is still high at 45%.

Source: Australian Treasury

Proposed tax cuts aim to alleviate cost-of-living pressures and may influence investment decisions. Understanding these dynamics is crucial for investors and policymakers navigating the evolving property market.

Conclusion: Navigating a Shifting Landscape

Australia’s property market in 2024 presents a complex picture. While the RBA’s focus on inflation control has led to higher interest rates, dampening buyer borrowing power, property asking prices remain resilient. This strength is likely due to the ongoing supply-demand imbalance and anticipated rise in migration.

The rental market faces significant challenges, with tight vacancy rates pushing rental yields upwards. This trend is likely to be further fuelled by strong migration, particularly in student-populated inner-city areas. However, some stability is expected for university-adjacent neighbourhoods due to continued student demand.

Limited new construction approvals further exacerbate the rental market strain. The proposed Stage 3 tax cuts, while aiming to ease cost-of-living pressures, may also influence investment decisions in unforeseen ways.

Understanding these dynamics is crucial for all stakeholders. Investors navigating this evolving market need to consider the interplay of interest rates, asking prices, rental yields, and potential tax implications. Policymakers face the challenge of balancing inflation control with fostering a sustainable housing market that caters to both homeownership aspirations and rental affordability.

The coming months will be crucial in observing how these various factors interact and influence the trajectory of Australia’s property market.